There’s a reason why home stagers prefer white or neutral colors when preparing a home for the market. Some colors can be distracting and a turn-off to home buyers.

Photo credit: Archideaphoto / Getty Images

Rethink a red-painted living room or dining area; red is the most off-putting color, according to a survey of home staging and design professionals conducted by the home remodeling site Fixr.com.(link is external) “Red is an extremely strong color and may not be to everybody’s taste,” the study notes.

Fixr’s Paint & Color Trends 2024 report flags the following as the most off-putting colors to home buyers:

Red: 53%

Lime green: 53%

Bright yellow: 40%

Mustard yellow: 19%

Pink: 10%

Turquoise: 9%

Instead of splashing interiors in bright hues, home stagers and designers say they like to use color strategically to warm up a space and even make it appear more spacious.

For example, 61% of experts recommend using warm neutrals—like beiges and whites—to help make small spaces appear larger. “Warm neutrals can reflect light and visually recede, and their calmness can make a space feel less overwhelming,” the study notes. White was a favorite among home stagers in making spaces seem more spacious and giving the illusion of higher and wider ceilings.

“When selling a house, paint and color trends need to be used in a softened way,” Birgit Anich of BA Staging & Interiors said in the Fixr study. The latest trends may call for attention-getting colors, but Anich warns that “a trend today is not necessarily the trend that buyers are yet ready to embrace. They need to have certain exposure to a new trend before they fall in love with the new trend. While these trends are great for interior design, they need to be used in a more moderate way when selling a property.”

Melissa Dittmann Tracey is a contributing editor for REALTOR® Magazine, editor of the Styled, Staged & Sold blog, and produces a segment called “Hot or Not?(link is external)” in home design that airs on NAR’s Real Estate Today radio show. Follow Melissa on Instagram and Twitter at @housingmuse.

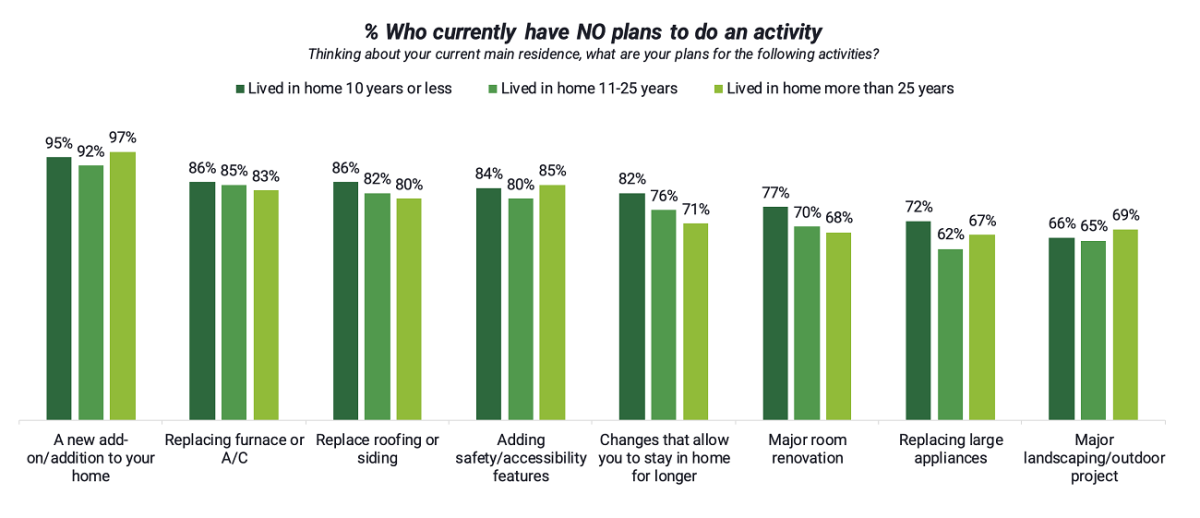

ShareMillennials are worried they’ll inherit properties in need of major renovations and repairs, which could further hamper affordability, a new survey shows.

Young move-up home buyers are growing increasingly worried that baby boomers, many of whom are staying put in their current home, won’t update their properties and will pass down costly renovations and repairs to the next generation of owners, according to a new study(link is external) from Morning Consult and Leaf Home, a national home improvement company.

Many baby boomers are choosing not to downsize, with 68% saying they’ve lived in their homes for 30 years or more, the study shows. Many in that group admit they’ve never done renovations or replaced major appliances—and they don’t have any plans to, either.

Source: “2024 Generational Divide in Homeownership Report,” Leaf Home/Morning Consult

Researchers say this could become a nightmare scenario for millennials, who may inherit or purchase these “time capsule” homes. Younger buyers’ budgets already are stretched thin by high home prices and mortgage rates. It’s difficult for many to add pricey renovations to their homebuying budget.

“The housing market is caught in a generational tug-of-war,” says Leaf Home CEO Jon Bostock. “Boomers will soon face aging-in-place hurdles, while millennials will face the surprise of homes in need of major updates. With an aging and ignored inventory of homes available in the next decade, we may see a crisis that will overwhelm the home improvement industry and strain the budgets of inheriting millennials, impacting the housing market.”

Taking More Than Their Fair Share?

Empty-nesters own twice as many large homes as millennials with children, 28% versus 14%, respectively, according to a new study from Redfin. But many young families need extra space: Millennials with children comprise about a quarter of three-bedroom-plus rentals in the U.S.—the largest share compared to any other generation.

Some millennials are waiting out the housing market for more larger homes that can accommodate their growing families. Ten percent of millennials say baby boomers are staying in their homes too long and should free up housing for them, the Morning Consult and Leaf Home survey finds.

But baby boomers, like many other homeowners, have little incentive to sell. Some may not want to give up the ultra-low mortgage rate they got in recent years while others own their home outright and are sitting on record amounts of equity.

Housing Experts: Crisis Looming

The aging housing stock in America is an issue that experts have been flagging for years. Economists are concerned about the impact aging homes could have on a housing market already struggling with a historic inventory shortage.The median age of an owner-occupied house is 40 years old, according to the American Community Survey. Slightly less than half of the owner-occupied homes were built prior to 1980; about 35% were built prior to 1970. As homes age, their components need to be replaced or repaired to keep them sellable. `A bloated, aging inventory of neglected homes could be the next big headache for the housing market, researchers warn.

Melissa Dittmann Tracey is a contributing editor for REALTOR® Magazine, editor of the Styled, Staged & Sold blog, and produces a segment called “Hot or Not?(link is external)” in home design that airs on NAR’s Real Estate Today radio show. Follow Melissa on Instagram and Twitter at @housingmuse.

ShareFrom ecosystem conservation to “new” darker neutrals in exterior paint, we look at the trends set to take hold in the industry next year.

Three Key Takeaways

Advise buyers that nobody should copy trends for their popularity since they change over time; a better approach is to seek joy.

Aging boomers have more options to choose among, from staying put with features that aid safety to going to a facility with specialized care.

Landscapes that conserve nature and shelter pollinators and wildlife are designed for private backyards and shared communities.

Staying abreast of what’s new and innovative in design and real estate is important, not to be trendy but to learn about innovative materials, systems and products to live more sustainably and benefit the planet. Also, new uses for rooms can maximize square footage and our surroundings to add joy to our lives. The following 10 trends are worth considering since they can positively influence whether homeowners reside in single- or multifamily housing.

Homeowners Are More Apt to Stay Put

With interest rates for a 30-year fixed mortgage still high, home prices holding steady and inventory still low, many homeowners plan to stay put, optimizing or expanding their existing square footage. Laurel Vernazza, Home Design Expert at The Plan Collection— Scarsdale, N.Y.-based company that sells pre-drawn plans—says that for those with no plans to move, the wish list includes:

Sustainable features

Accessory dwelling units as zoning laws change

Pickleball courts

Remodeled basements with saunas

Media centers and game rooms

Home offices as working from home continues

Outdoor space, not just at ground level but above as well

AI-driven technology to make homes easier to use and more energy-efficient

Why now? Homeowners want to be active but decrease maintenance and energy consumption. They favor sustainable materials sourced locally to pare carbon footprints and support local businesses, which is especially true for millennials and Generation Z. Many materials reflect better waterproofing, and garages may have room for battery back-up systems if power goes out, says architect Jonathan Boriack, AIA, LEED AP, principal with KTGY in Oakland, Calif.

Specialized Needs for an Aging Population

Architectural firms like The Architectural Team (TAT) outside Boston are designing facilities for specialized needs, such as The Cordwainer, which will have private and double rooms and a host of amenities including a two-story atrium, performance center, game room to stimulate the brain, and memory care garden. The bedrooms will be divided between two neighborhoods so residents can safely wander, says TAT architect Anthony Vivirito. Also critical is light to help with circadian rhythms and mood. “Biophilic elements and the focus on unique spaces for invigorating activities and entertainment required stepping away from traditional practices,” says Tamilyn Liesenfeld, president and CEO at Anthemion Senior Lifestyles, which owns and operates The Cordwainer in Norwell, Mass.

Why now? With aging boomers numbering 76.4 million, more attention is paid to their housing needs when they can’t stay at home, which includes many of the estimated 6.7 million who have Alzheimer’s disease.

Smaller Single-Family Homes and More Townhomes

Variety is the spice of homebuilding. Currently, homes are shrinking in size(link is external), with the median for single-family houses at 2,261 square feet and the mean square footage of new single-family homes down to 2,469, according to the National Association of Home Builders. One of the most popular styles is the ranch house. The style also offers the flexibility to be opened up indoors and to the outdoors, according to Vernazza. Attached townhomes and stacked flats have gained popularity due to the need for smaller square footage in dense sites, says Boriack.

Why now? The main reasons(link is external) for smaller single-family homes are high mortgage rates and lifestyle changes that favor fewer bedrooms. As far as townhomes and stacked flats are concerened, the economics of for-sale property works with current market finances more for developers than rentals do. Land shortages make attached and stacked units smart choices.

Bigger Apartments

At the same time that single-family homes are shrinking, apartments are increasing from an average of 870 square feet before the pandemic to closer to 1,000 square feet, says architect Sean M. Stadler, FAIA, LEED AP, a managing principal with WDG Architecture’s Washington, D.C. office.

Why now? Many renters want more space to work from home and favor more bedrooms, if they can afford, Stadler says.

Homeowners Want Sustainable Energy Use

Sustainability isn’t going anywhere. In fact, it’s growing in popularity, and received a boost in January 2023, when the Department of Energy(link is external) announced federally backed incentives to help builders make DOE-certified Zero Energy Ready Homes their standard. An example of a builder focused on both energy efficiency and lower construction waste is Netze Homes, based outside Dallas, which uses steel that it recycles from cars. It claims its houses are 20 times stronger than those built from wood. Since the frame is built in a factory to exacting specifications, the homes are tighter and the resulting lower air exchange makes them more efficient.

Why now? Sustainable homes do a better job of withstanding extreme weather, are fire-resistant, and curb termite damage, wood rot and mold. Energy-efficient homes help residents save up to 35% on their electric bills and cut 40% of waste since the frame is formed in a factory. These homes have lowered carbon emissions by 50% against the industry average, proponents say.

Luxury Spec Building Demand is on the Rise

The demand for spec luxury houses and townhomes continues, particularly in South Florida, according to J.C. de Ona, president of the southeast division of Centennial Bank. Waterfront sites are particularly desirable. “Some demand may have softened so that there now may be 10 to 20 buyers rather than 100 at a house, but it’s still strong and prices remain up,” he says. Favored features include a modern design with flat roofs, wood detailing, a pool, an open plan and beautiful kitchens, he says.

Why now? After slowing from 2012 to 2014, spec building has picked up, due to an uptick in migration. Jose R. Boschetti Jr., managing partner of The Boschetti Group in South Miami, Fla., also sees demand from buyers wanting a minimalistic design and maintenance-free living with artificial turf, porcelain floors, smart features and pools in close proximity to the house to maximize indoor/outdoor connection.

An Abundance of Multifamily Amenities in Small Buildings

People are still looking for features in smaller buildings, says architect Joshua Zinder of Joshua Zinder Architecture + Design in Princeton, N.J. His four-story, six-unit, mixed-income building, Nelson Glass House, reflects the trend of “amenity creep” that has “percolated down to smaller buildings,” he says. Units have terraces, shared parking, bike storage, “Zoom rooms” for online meetings and a ground-level coffee shop. “Having just a good location doesn’t cut it anymore,” he says. Other popular amenities, he says, are a grocery store, pet trail, package center, and lounge and lobby for interaction—sometimes with classes—and electric vehicle charging stations.

Some buildings use amenities like EV stations to add revenue, according to Swtch Energy, an EV charging solutions provider that works with multi-tenant properties. Many buildings add programming through a property management company like FirstService Residential, says Katie Ward, the company’s regional president for Texas. The trend has evolved that property management doesn’t just plan space but creates a culture to tailor connections to needs through events, she says.

Why now? Amenities allow smaller buildings to compete with bigger ones, retain residents and attract newcomers, says Stadler. One challenge is having amenities that are appealing when a building opens, since the timeline for delivery may be five years.

A Continued Focus on the Kitchen

The kitchen remains the heart of the house with old trends in force along with new ones gaining traction, says designer Mick De Giulio of de Giulio Kitchen Design outside Chicago. Induction cooktops continue to increase in number, in part because new homebuilding regulations in certain municipalities require phasing out gas ranges for safety and sustainability, according to The Plan Collection.

De Giulio says an organized, walk-in pantry; more light through big windows or LEDs in warmer colors; artisan and hand-crafted features such as hand-scraped wenge wood; and a mix of materials like German silver, stainless with special finishes, and bronze are popular, as well as the island.

Why now? In most cases, the kitchen is one of the most used, most seen rooms in a home. People are still eager to congregate in the kitchen, and within the space, certain trends stand out. A kitchen redo makes sense since, if it’s done well, it can last 30 years, though appliances may need to be replaced along the way, De Giulio says.

Natural, Native Landscaping as a Priority

Whether in communities or private backyards, homeowners want to conserve ecosystems. In smaller communities, even in urban settings, variations of the conservation community or “agrihood,” like Pendergrast Farm in Atlanta, are emerging. The 20 energy-efficient, solar panel–ready homes, wired for EV charging stations, will have a Home Energy Rating System rating of 50 that will use 50 percent less energy than comparable new homes. Seventy percent of its land will be preserved for woods and a working farm.

In private backyards, “rewilding” uses native plants to create habitat. Hillary Peters with Mariani Landscape in Lake Bluff, Ill., says this trend is popular among clients who are interested in restoring ecosystems and biodiversity. By bringing native plants to a landscape, homeowners can create a space that meets needs and supports wildlife.

Why now? Such communities bring together features that reflect homeowner interest in conservation, and the scarcity of land makes this viable. Likewise, homeowners are aware of their impact on their environment and the need to protect wildlife. Any little bit helps, Peters says—installing a birdhouse or water feature or using native plants and grasses makes a difference.. She advises against cultivars, which do not always serve pollinators.

“New” Neutrals for the Exterior

Neutral colors are more popular, says residential and commercial color consultant Amy Wax in Montclair, N.J. “They are a safe choice, offer the opportunity to decorate a home with more emphasis on landscaping, give homeowners the chance to market their home without having to repaint and are not the subdued hues of the past,” she says. Many neutrals are even darker, such as midnight blue, charcoal gray and true black for drama.

Why now? Dark exterior accents express confidence with a bold street presence. Adding a periwinkle blue front door or taxicab yellow or hot pink accent is fair game. Durability should be weighed since darker colors may fade, so it’s best to apply paint with a subtle sheen to protect surfaces.

Homeowners who decline to use a real estate agent to sell their property are twice as likely to say they weren’t satisfied with the selling experience, according to a new survey from Clever Real Estate(link is external) of 1,000 home sellers in 2022 and 2023. Survey respondents say they realize they likely made less money on their home sale and faced more stress by not having a professional representative.

Those who didn’t use a real estate agent said before their transaction that they think pros are overpaid for what they do and are not more knowledgeable about the homeselling process than the average seller. However, when these respondents reflected on their experience after the transaction, they admitted that they made some mistakes without the help of a pro.

More than a third of non-agent sellers, such as FSBOs or those selling to an iBuyer, said the process was more difficult than they expected. What’s more, these sellers admitted:

Buyers distrusted them because they didn’t have an agent (43%).

They struggled to understand their contract (40%).

They made legal mistakes because they didn’t use an agent (36%).

The survey also found other consequences of going it alone as a seller:

Lower sales price: Homeowners who sold without a real estate agent are three times more likely to say they lost money on their home sale. The Clever Real Estate survey found that those who sold their home with an agent tended to earn $46,603 more in average profits than those who sold without an agent in 2022 and 2023. About half of unrepresented sellers say they wish they had priced their home differently, and nearly half now believe their home would have sold for more if they would have used an agent.

Longer selling process: Home sellers without an agent are nearly twice as likely to say they didn’t accept an offer for at least three months; 53% of sellers who used an agent say they accepted an offer within a month of listing their home. Ironically, many homeowners who didn’t use an agent said the primary reason for going it alone was to sell faster.

More stress: Half of home sellers who did not use an agent admit to crying at some point in the process. Fifty-two percent of unrepresented home sellers said they felt overwhelmed by the entire sales process. On the flip side, homeowners who hired an agent were more likely to say they felt good about their sale and expressed less stress.

To be fair, home sellers who used an agent also had some gripes about their experience, albeit much fewer. But those who were unhappy with their agent experience expressed feelings like their agent was only looking to make a sale and didn’t care about their interests, their agent “annoyed” them, or they thought the agent pressured them into decisions, the survey found. That said, 77% of respondents who used an agent say they were satisfied, and 72% say they would use their agent again.

Even as the vast majority of home searches start online, most consumers still use real estate agents to buy or sell a home. Indeed, the National Association of REALTORS®’ 2023 Profile of Home Buyers and Sellers found that 89% of buyers and sellers in the last year used a real estate agent, up from the previous year.

Only 7% of homeowners sold as a FSBO over the last year—which matches the all-time low recorded in 2021, according to NAR data. FSBOs continue to not fare as well in the market as professionally represented homes: FSBOs sold at a median price of $310,000 in the last year, compared to $405,000 for listed homes, NAR’s data shows.

“Having a REALTOR® help you navigate the homebuying and selling process provides peace of mind, especially in a challenging market with high prices, elevated mortgage rates and limited inventory,” says NAR President Tracy Kasper.

Melissa Dittmann Tracey is a contributing editor for REALTOR® Magazine, editor of the Styled, Staged & Sold blog, and produces a segment called “Hot or Not?(link is external)” in home design that airs on NAR’s Real Estate Today radio show. Follow Melissa on Instagram and Twitter at @housingmuse.

ShareFall is the time to get organized. Help clients figure out how to store and stash their belongings with these best practices.

3 Key Takeaways:

Storage options should reflect a homeowner’s needs

Make sure to include storage options in every room

Keep storage placement, pricing and ease of use in mind

New homes are shrinking in size and storage space, and older homes have their share of storage woes as well, which makes it difficult for homeowners to keep their homes tidy and organized.

Though many homeowners in recent years have latched onto the decluttering philosophies of Marie Kondo and Swedish Death Cleaning, some didn’t organize and store what was left, leaving them with piles. Moreover, most homeowners continue to buy, making it unlikely that their rooms will have space for everything.

Designer Jacob Laws of Jacob Laws Interior Design and his partner know the trials of limited storage space. They own an early 1800s home in Charleston, S.C., and intentionally limit their possessions to ensure it stays tidy. “But it’s easier for us,” he says. “This is what we do professionally.”

The good news is that everyone from home builders and architects to professional organizers and designers are swooping in to help.

Commercial interior designer Mary Cook of Mary Cook Associates, who advises homebuilders, is seeing bigger closets emerge. Jeff Benach, principal of Lexington Homes, has altered the angle of a staircase in one townhouse model to accommodate a second hall closet and also angled the garage to make its ceiling higher to fit more storage. Wingspan Development Group offers extra closets as options in some of its multifamily units, including walk-in styles and pantries off kitchens. Many pros such as salesperson Aleks Videnovic of Compass, a founder of StageIT.site and RenderPRO.io, make visualizing possibilities easier with renderings.

Fall is a good time to encourage clients to organize their storage, and a few best practices can help so the task doesn’t become overwhelming. Doing so also helps when they sell since well-planned storage shows buyers how their houses can work efficiently, says Allison Bond, a salesperson with Cummings and Co. Realtors, which is headquartered in Maryland.

Best Practices

Before organizing, homeowners should declutter, basing their decision on the traditional rule of if something hasn’t been used in three to five years or offers great sentimental value, it goes.

Figure Out How and Where

Every homeowner should factor in how long they hope to stay since built-ins, including closet systems, can be more costly than many freestanding furnishings, which may be transported to a future home. “Live in your space for a few months before you commit to any storage investment,” Laws says.

The best questions for homeowners to ask themselves, says architect Bob Zuber, AIA, principal at Morgante Wilson Architects, are: What am I storing? How accessible does it need to be based on frequency of use? Does what’s being stored involve special considerations such as temperature control?

Trends come and go. Big entertainment centers and armoires are passé while “Costco Closets” in suburban homes for bulky items are now in, Cook says.

Any systems installed should be adjustable whether shelves in a bookcase or clothing rods in a closet since needs change.

Keep It On Brand, But Not Personalized

Storage should reflect a home’s design style and price point, which means more expensive wood shelves rather than wire in mid-priced to luxury homes.

Think carefully about which materials to use. In general, metal costs more than wood, except for exotic species; stained wood is more expensive than painted; and melamine and similar materials are the least expensive yet still very durable, says designer Rebecca Pogonitz of GoGo Design Group. Wood offers the advantage of being able to be customized, says designer Suzan Wemlinger, principal of Suzan J Designs.

Homeowners should avoid over-personalizing storage unless what’s stored warrants extra expense. This rule may apply to a fine wine collection in a custom cellar. An alternative is a refrigerated wine cooler that can be taken to another home.

Keep the Space in Mind

Storage should never be placed so it blocks doors, windows, furnishings and traffic flow; its purpose is to support daily life rather than make it harder.

Future needs should be considered by not filling up every storage option. That happened during the pandemic when many homeowners hunted for space for a home office. Some found it by converting an extra closet into a functional cubicle.

Off-site public storage should be avoided when possible since it’s costly and often becomes an excuse for delaying decluttering, says Videnovic.

Every room should have some storage. “People will notice if there’s none,” says Amanda Wiss, a stager, organization expert and founder of Urban Clarity.

ShareKnow what entices buyers and what needs to go when it comes to smart home features.

When it’s time to sell a smart home, unique considerations come into play. This article will take you through essential steps to successfully selling a home outfitted with smart technology, using insights from a home that was recently listed for sale.

Decide What Stays and What Goes

The first step in preparing a smart home for sale is determining which devices stay with the home and which go with the seller. Some features are considered personal property, like hubs and voice assistants. Some automations and features may not work without the hubs or an active account that is connected to the internet. These are the items sellers would take with them.

Other features are considered a value-add and are big draws for buyers. Video doorbells, for example, are generally recommended to be left behind, providing an attractive feature for the next homeowner. Likewise, smart thermostats, switches and locks are big draws for buyers. These are usually better left behind, with sellers understanding that they can purchase a new one for their next home.

When you’ve determined what will stay and what will go, make a thorough inventory of all smart products in the home, with the aforementioned determination clearly noted by each product. Items that connect to the internet need to be reset for the new owner. Creating a complete listing of these items ensures a clean handoff.

Factory Reset and Privacy

Before listing, a seller will want to think about they want to leave behind and what they want to take with them. A smart lock, for example, is a device that sellers might leave behind. If they do, they must reset the master code and ensure the new owner can reconnect it to a new Wi-Fi network.

When dealing with devices that have a master code written on them, as some smart locks do, ensure this is covered or the device is secured. Always factory reset all smart devices so the next owner can maintain their privacy and set them up from scratch. Sellers may need to do this using the device’s app while it is still connected to the seller’s home network.

Future-Proofing

Smart homes often include infrastructure designed with the future in mind, such as wiring for a security system or Ethernet. When selling, ensure that prospective buyers are aware of these features, as they represent significant value. Even setups for potential future additions, like a NEMA 14-50 outlet for a potential electric vehicle charger, can be a selling point, especially for buyers considering an electric vehicle in the future.

Determine Value

Evaluate whether certain smart features add value to the home or are better off removed. For instance, smart locks, doorbells and thermostats generally enhance a home’s appeal, while buyers generally have varying opinions on security cameras or smart lighting.

In some instances, the cost of removing and replacing certain features, like smart switches, may outweigh the benefit of taking them to a new home. These switches can often still function as regular dimmers even without the smart capabilities, providing added value for the new owner whether they want to make use of the smart feature or not.

Selling a smart home is a process that calls for careful consideration of what adds value and what needs to be reset or removed. By following these steps, agents can help ensure a smooth and successful sale, benefiting both the seller and the new owner.

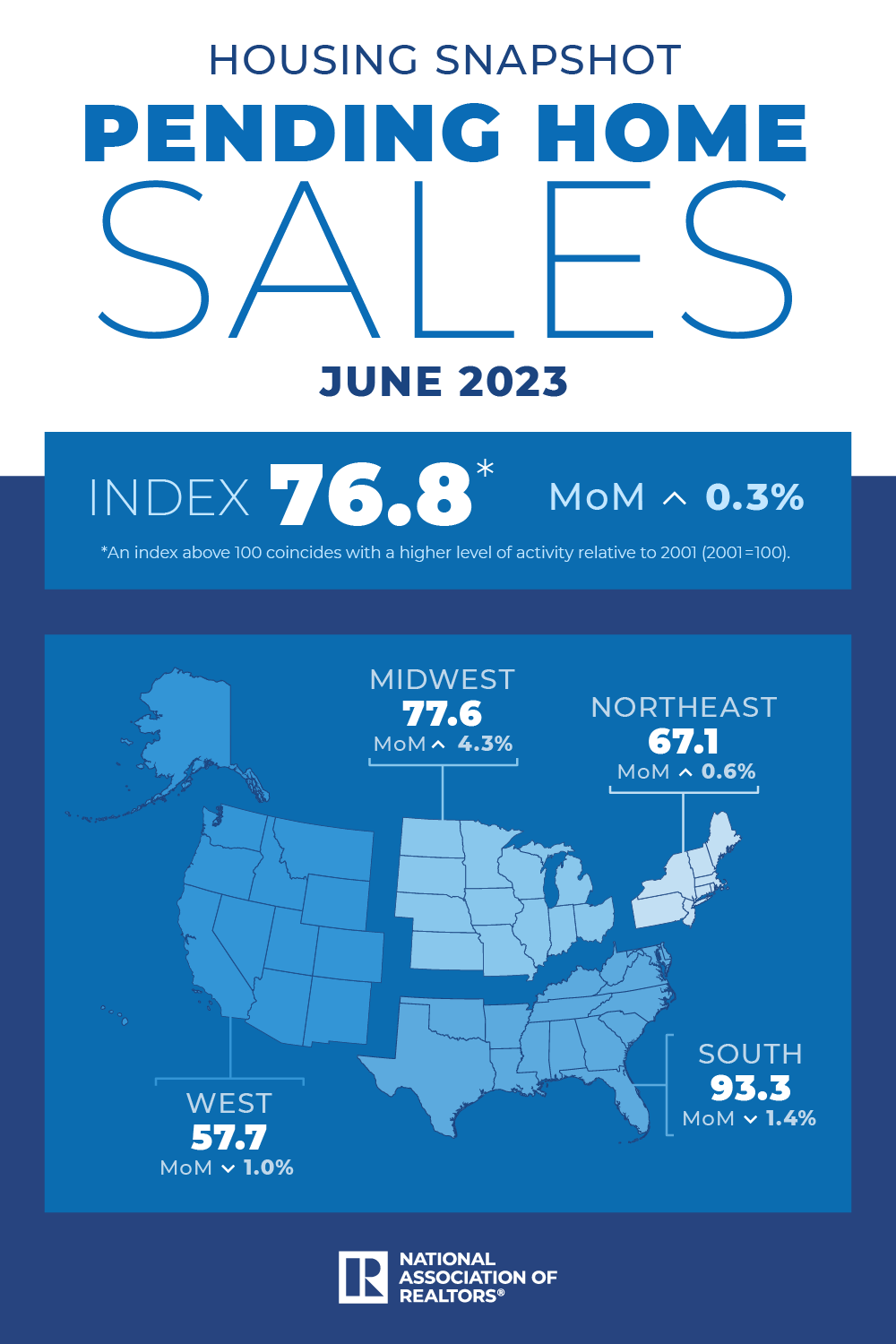

Contract signings picked up the pace last month, and home buyers are increasingly facing multiple offer situations. NAR releases its housing forecast for the remainder of the year and 2024.

Pending home sales rose slightly in June, and the latest indicators are showing a housing market on the mend. Median existing-home sales prices in June soared to their second highest on record in the last two decades, and more buyers are facing multiple offer situations once again, the latest reports from the National Association of REALTORS® shows. NAR’s Pending Home Sales Index—a forward-looking indicator of home sales based on contract signings—rose 0.3% in June, the first increase in four months.

“The recovery has not taken place, but the housing recession is over,” says Lawrence Yun, NAR’s chief economist. “The presence of multiple offers implies that housing demand is not being satisfied due to a lack of supply. Homebuilders are ramping up production and hiring workers.”

Housing inventories remain at historical lows, down 13.6% from even last year’s low levels. “There are simply not enough homes for sale,” Yun said in a recent report. Seventy-six percent of existing homes sold in June were on the market for less than a month, NAR’s data shows.

Home buyers are faced with limited choices, higher home prices and higher mortgage rates. But they may find some relief soon: Mortgage rate increases may be mostly over, and that would bode well for home-buying, Yun says.

“With consumer price inflation calming close to the Federal Reserve’s desired conditions, mortgage rates look to have topped out,” Yun says. “Given the ongoing job additions, any meaningful decline in mortgage rates could lead to a rush of buyers later in the year and into the next.”

NAR forecasts that the 30-year fixed-rate mortgage could reach 6.4% by the end of the year, followed by 6% in 2024. Over recent weeks, mortgage rates have been nearing 7%, far from their ultra-low 2% or 3% averages just over a year ago.

Home Sales Outlook

NAR released its latest forecast showing what they believe will be the trajectory of the market over the coming months:

Existing-home sales: NAR predicts existing-home sales to fall 12.9% in 2023 compared to 2022, and then climb by 15.5% in 2024.

Prices: National median existing-home prices are expected to remain mostly steady, likely ending this year just 0.4% down compared to 2022, reaching $384,900 for 2023. Home prices are then expected to rebound by 2.6% in 2024 to $395,000, NAR predicts. The West—the nation’s priciest region—likely will see prices reduced more, while more affordable regions, like the Midwest, are forecasted to post moderate increases, NAR’s report says.

New-home sales: Sales of newly constructed homes are forecasted to be a bright spot for home sales, as more buyers search for greater inventory options. New-home sales are expected to rise by 12.3% in 2023, and by another 13.9% in 2024, NAR predicts. The national median new-home price is expected to fall by 1.9% this year, to $449,100, before jumping by 4.2% the following year to $468,000.

Housing construction: Economists have been calling on the new-home market to make up for the supply deficits in the real estate market. But NAR is forecasting that housing starts will fall 5.2% in 2023 compared to 2022 (reaching 1.47 million). Housing starts are expected to ramp up in 2024, however, rising 5.4% to 1.55 million.

“It is critical to expand supply as much as possible to widen access to home buying for more Americans,” Yun says. “Home prices will be influenced by how much inventory is brought to market. Increased homebuilding will tame price growth, while limited construction will lead to home price appreciation outpacing income growth.”

Regional Breakdown on Contract Signings

Meanwhile, the latest housing market conditions show a market much slower than last year’s brisk pandemic-fueled pace. Overall, pending home sales were down in June by 15.6% compared to last year, NAR’s data shows. But market performance did vary regionally. Month over month, contract signings increased in the Northeast and Midwest, while falling in the South and West. Nevertheless, all four major regions of the U.S. posted year-over-year decreases in transactions in June.

Melissa Dittmann Tracey is a contributing editor for REALTOR® Magazine, editor of the Styled, Staged & Sold blog, and produces a segment called “Hot or Not?(link is external)” in home design that airs on NAR’s Real Estate Today radio show. Follow Melissa on Instagram and Twitter at @housingmuse.

ShareFind out what home styles—both interior and exterior—are seeing dramatic increases in online searches.

Homeowners are trying to maximize their space by taking on remodeling projects geared toward creating new living areas while overhauling their property’s style, according to the 2023 Houzz U.S. Emerging Summer Trends Report. Houzz, a home improvement site, analyzed the latest search insights from homeowners, designers and contractors to identify the following top trends.

Online searches for “finishing a basement” have increased significantly over the past year as more homeowners look to turn their large, open spaces into a family or recreation room. Basements are being refinished to create a spot for watching movies, playing games and exercising, according to the report. The search term “basement golf simulator” posted one of the biggest upticks among home improvement-related searches, the report shows.

More homeowners are looking up to expand their spaces. Houzz found that “rooftop deck” and “rooftop patio” searches increased by 90% and 40%, respectively. The trend is mostly occurring in metro areas where outdoor space is a hot commodity, the report notes.

More homeowners are showing an interest in renovating their bathrooms to include accessible features that enable them to live in their homes longer as they age. Houzz found that searches for “age-in-place bathrooms” and “handicap-accessible bathrooms” more than doubled compared to a year ago. Popular add-on features include handheld shower heads, ADA-compliant bathroom vanities and curbless showers.

A greater number of homeowners are showing a desire to swap out their pristine, all-white kitchens for something a little more rugged. “Industrial kitchens” are generating greater interest, particularly for features like “kitchen track lighting,” “pull-down kitchen faucets,” “stainless steel countertops” and a “brick kitchen wall.” Houzz researchers also noticed a growing interest for “concrete countertops” and “copper kitchen backsplashes” that fit within this style.

More than half of renovating homeowners surveyed say they’re designing their kitchens for entertaining. Searches over the past year have grown for “open-concept kitchen to family room” and “island cooktop and ranges,” the survey says. These features allow hosts to prepare a meal as they engage their guests. Searches also have doubled for a “walk-in kitchen pantry,” with a space to not only tuck away kitchen goods but also hide toasters, coffee makers and other smaller appliances.

Open-concept design is popular in the kitchen, but homeowners still desire some privacy. Houzz researchers saw an uptick in interest in design elements that create temporary separation like a “living room divider,” “Shoji screen” or “partition wall.”

The fifth wall is becoming the new place for an accent wall. Paint and texture are dressing up more ceilings. The trends report shows searches have spiked over the past year for “high-gloss ceilings,” “painted ceilings” and “black ceilings.” “Tongue-and-groove ceilings”—which are wooden planks that fit side to side across a ceiling—are also up significantly, with searches growing by 73% over the past year, Houzz reports.

Classic architectural elements are being mixed in with contemporary ones. Notably, search trends are up for features commonly associated with Colonial and Spanish Colonial styles. For example, homeowners are searching for Colonial design elements like “front porches” and “formal living rooms” as well as “Spanish Colonial exteriors.” “Homeowners are hiring architects and designers to help them honor the roots of their homes, while updating them with a cohesive, intentional look,” the report says.

Homeowners are making the most of their outdoor space and aren’t letting limited size shrink their plans. Searches for “small swimming pool,” “small plunge pool,” “small pool house” and “small screened-in porch ideas” grew over the past year, the report notes. Also, researchers report that searches for “small outdoor kitchens” have more than doubled over the past year.

Melissa Dittmann Tracey is a contributing editor for REALTOR® Magazine, editor of the Styled, Staged & Sold blog, and produces a segment called “Hot or Not?(link is external)” in home design that airs on NAR’s Real Estate Today radio show. Follow Melissa on Instagram and Twitter at @housingmuse.

The most important rule when it comes to furnishing a home is that there is a distinct difference between decorating a house to live in versus staging a home to sell. Sounds much the same, but one key factor makes these two décor styles very different: personal preferences work well for owners but not necessarily for potential buyers. Staging to sell, just like curb appeal, has always been important, but current data shows that getting it right is more important than ever.

When staging a home to attract potential buyers, we really don’t know their personal preferences, so custom styling isn’t an option. On your initial walkthrough of the property, determine the style of home—whether it’s a colonial, farmhouse, Cape Cod, contemporary, etc.,—and assess the neighborhood’s features (family-friendly, first-time home buyers, retired community) and go from there. These staging tips should get you started.

Neutral Palate

The safe bet is to keep all décor a neutral shade, with no vibrant colors that might be an eyesore to potential buyers. You want well-fabricated furnishings that don’t feel cluttered so as not to make the home appear smaller potentially. Regarding furnishings, take a minimal approach and remember: quality over quantity makes the difference.

Declutter

This brings me to the next tip; don’t over-accessorize the home! Allow the property to feel open and airy. Too many items can feel messy and, worst of all: unkempt. Your goal is to allow the potential buyer to be able to envision themselves in the home, with their own personal property in there so kitchen countertops, living areas, garages and especially outdoor spaces like backyards and patios. Keep things neat and tidy. If needed, see if the current owner can remove and store their belongings if there are too many.

Artwork

Here size does count. The bigger, the better. Instead of filling your walls with floating shelves or a dozen small picture frames that can look busy, opt for 1-2 oversized paintings or exclusive prints that fill the space. Note: choose artwork that’s preferably not from HomeGoods where there’s a multiple of the same. If budget is a factor, check out Esty or local vintage stores for more unique, one-of-a-kind pieces to give the home an elevated touch.

Lighting

Make sure all your lighting is the same color. There’s nothing more off-putting than walls and rooms looking different with different shades of light. Check bulbs and fixtures to make sure everything matches up and is in working order.

Drapery

This is a big one if you want to elongate the room and create a touch of elegance. The rule is to go from ceiling to floor and not window height to make the ceiling height appear higher. Remember to keep the neutral palette in mind, but you want to make sure you’re not washing out the room with window treatments. It’s a fine balance, so don’t be afraid to try a couple of options before settling on something.

Scent

We’ve all heard the saying that “first impressions last.” Well in the case of scent, it’s absolutely TRUE! To help a home give off the right vibe, make sure you have a pleasing scent throughout the home. Some tried and tested favs: clean linen, floral, pine/fir. It’s also a great way to neutralize any smells—cooking, pets, etc.—that might have been lingering. Burning a candle an hour before having company removes any odors and sets up showings and open houses for success.

Bedrooms

Bedrooms are an important part of staging and not to be forgotten. Potential buyers almost always place emphasis on the bedrooms, especially the main one. In this space, the bed is the focal point, so that’s where you want to maximize your efforts. To create a luxe feel, opt for white linens with huge, full cushions and make sure the bed is wrinkle-free. If there’s a large wall above the bed, make sure to use some oversized artwork when possible, and if there’s a window above the bed, follow the drapery tips to bring the space together.

Bathrooms

Bathrooms need to look clean and fresh. Again, using white gives that touch of elegance. Your instinct might be to hang towels on the towel racks, but for a well-kept, clean and tidy look, fold them instead and place them in a basket. Surfaces should be clean and dry, and make sure any touches like shower curtains and rugs make the space feel light and airy.

Remember that when staging a home, the goal is to create a space in which potential buyers can imagine themselves. Once staged, walk through the space as though you are a client, and visualize the home as though you’re seeing it for the first time. Use these staging tips and keep an open perspective, and you won’t go wrong!

Monika Bhondy was born Brit who moved to North America and now resides in the Chicagoland area. Monika comes equipped with vast life experiences with over 20 years of experience in the service industry under her belt. Her attention to detail, a keen eye for esthetics and uncanny ability to connect with others has seen her passion for styling evolve into a lucrative real estate business. A licensed REALTOR® since 2016, Monika accomplished $2 million in sales in her first four months in the industry, earning her Million Dollar Guild™ status, which she has held since 2017. She’s a Certified Luxury Home Marketing Specialist® and a member of the Institute of Luxury Home Marketing™. Want to know if your home is priced right? As a Pricing Strategy Advisor, she’ll get you there. One of the few real estate professionals who is also a Certified Staging Consultant (held by less than 1500 brokers in Illinois as of 2020), she proves her passion for exquisite styling and knowing what works is always on point.

**NOTE: Evidence of payment for all Advance Sales in the form of vouchers or payment confirmation must be presented at Gamble High School the day of the tour to exchange for ticket

Parking information available at the school. Epworth Avenue lot is for ticket pickup parking only.

Shuttle buses are NOT availlable.

Questions? See FAQs or email info@Westwoodhistorical.org or leave a message at 513-268-7066

==== HOUSE SPONSORS ====

Frond, Hoeting Realtors, Maple Knoll Communities, Adam Sanregret – Keller Williams,